Reconciling in bookkeeping means comparing your internal financial records to external documents, like bank statements, to ensure they match. It helps maintain accurate financial reporting, detect discrepancies, and avoid costly mistakes.

What Does Reconcile Mean in Bookkeeping?

Reconciling in bookkeeping means ensuring your internal financial records match external statements like bank records or invoices. This essential process identifies and corrects any errors, making sure that your books reflect the real financial situation of your business.

At Careers Collectiv, we emphasise the critical role that reconciliation plays in maintaining trustworthy and accurate financial statements, no matter the size of your organization.

What Is Bookkeeping Reconciliation? (Meaning and Purpose)

Bookkeeping reconciliation is the process of comparing internal records against external sources to verify that every transaction aligns accurately.

- Simple definition: It’s double-checking that what your business recorded actually happened in the real world.

- Purpose: Bookkeeping reconciliation ensures that your financial statements match real-world transactions, safeguarding your business against errors, fraud, and financial misstatements.

Why it matters:

- Catch mistakes early before they compound

- Validate the accuracy of financial statements

- Build confidence for audits, investors, and internal reviews

Why Is Reconciliation Important for Bookkeeping and Accounting?

Reconciliation isn’t just another accounting task; it’s a frontline defense for financial health. It ensures that transactions match across records and bank statements, helping to catch errors and prevent fraud. Naturally, this process highlights the importance of financial accuracy, which leads many to ask: what is the difference between bookkeeping and accounting? Bookkeeping focuses on the day-to-day recording of financial transactions, while accounting involves interpreting, analyzing, and reporting those transactions to support strategic decisions. Reconciliation connects the two by verifying that the recorded data is accurate and complete.

Detecting and preventing accounting discrepancies:

- Small errors can snowball into major financial reporting issues. Regular reconciliation spots mistakes early.

Ensuring financial compliance and audit readiness:

- Whether for tax season, external audits, or regulatory compliance, accurate books are non-negotiable.

Preventing fraud and errors in financial statements:

- By cross-referencing transactions, you can detect unauthorised activity or internal fraud.

Different Types of Bookkeeping Reconciliation

Reconciliation isn’t limited to your bank account. Several critical types exist.

Bank Reconciliation:

- Matching your business’s ledger with your bank statement, verifying deposits, withdrawals, and ending balances.

Vendor Reconciliation:

- Ensuring supplier invoices and payments match recorded payables.

Customer Reconciliation:

- Confirming that accounts receivable match customer payments.

Inventory Reconciliation:

- Aligning recorded inventory counts with physical stock.

Intercompany Reconciliation:

- Matching transactions between different branches, divisions, or subsidiaries.

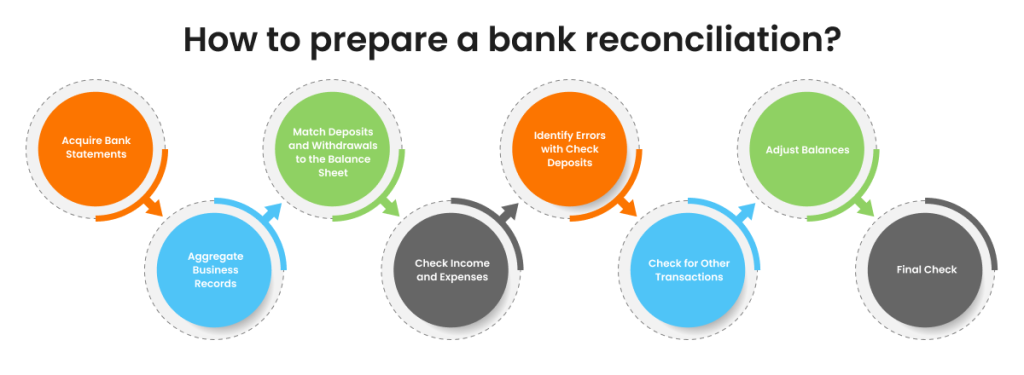

Step-by-Step Guide: How to Reconcile Accounts in Bookkeeping

Step 1: Collect documents and records

- Gather internal ledgers, receipts, bank statements, and invoices.

Step 2: Match each transaction

- Compare the data between your books and external sources line-by-line.

Step 3: Identify and explain discrepancies

- Investigate mismatches, missing transactions, or timing issues.

Step 4: Correct errors and adjust books

- Amend any recording errors and document corrections.

Step 5: Confirm matching balances and close

- Once records align, finalise reconciliation for the period.

Tools and Software to Simplify Bookkeeping Reconciliation

Technology makes reconciliation faster and more accurate.

Introduction to bookkeeping software:

- Programs like QuickBooks, Xero, and FreshBooks automate much of the matching process.

Benefits of automated reconciliation:

- Reduced manual errors

- Saves time during month-end close

- Provides real-time financial visibility

How integrated systems improve reconciliation accuracy:

- Integration between sales systems, banking, and accounting creates seamless financial data flow.

Common Reconciliation Mistakes (and How to Avoid Them)

Even seasoned bookkeepers sometimes make mistakes during reconciliation.

Delayed reconciliations:

- Waiting too long can lead to forgotten details and more work.

Ignoring minor discrepancies:

- Small differences can hint at bigger problems later.

Not reconciling all accounts:

- Some businesses focus only on bank accounts and forget credit cards, loans, or petty cash.

Manual entry errors:

- Typos or missed transactions can throw off entire reconciliations.

Best Practices for Bookkeeping Reconciliation Success

Make reconciliation second nature to your bookkeeping routine.

Set a monthly or quarterly reconciliation schedule:

- Stay ahead of potential issues by reconciling consistently.

Use checklists to track reconciliation tasks:

- A simple list prevents missing key steps.

Assign responsibility clearly between team members:

- Designate who reconciles which accounts.

Document every discrepancy found and corrected:

- Maintain transparency and a clean audit trail.

Frequently Asked Questions About Bookkeeping Reconciliation

How often should you reconcile your accounts?

Ideally, monthly. Quarterly at a minimum to catch discrepancies early.

Can reconciliation be fully automated?

While software can automate much of the process, human oversight is still essential.

What if I can’t find the cause of a discrepancy?

Investigate thoroughly. If unresolved, consult an accountant or audit your processes.

Do small businesses need to reconcile monthly?

Absolutely. Small businesses benefit greatly from regular reconciliations to manage cash flow and prevent mistakes.

Importance of Regular Reconciliation

Maintaining financial accuracy through regular reconciliation isn’t optional—it’s vital for business success.

At Careers Collectiv, we encourage businesses of all sizes to make reconciliation a priority, supported by reliable bookkeeping practices or smart automation tools. Ensuring your financial statements match real-world transactions today prevents bigger problems tomorrow.

When you commit to reconciling financial records regularly, you strengthen the foundation of your business’s financial future.